Mini/Micro LED has not yet been mass-produced on a large scale, which is not unexpected. Fortunately, though the production of the other side is still far away, the path has gradually become clear. In 2022, under the headwind of the macroeconomic environment, Mini/Micro LED was faced with challenges but new opportunities as well. Whether it is the technology and cost issues of the industrial chain or the application and demand of the terminal, there will be solutions to release some tense.

MiniLED backlighting: 6 distinct applications

Among the new display technologies, MiniLED backlighting is the first to be implemented on a large scale, and has now formed a relatively complete industrial chain covering equipment, materials, chips, devices, modules, panels, and more. In recent years, driven by strong promotion from brands and the industrial chain, MiniLED backlighting products have opened up a wide range of application scenarios, including consumer electronics and IT products such as TVs, monitors, laptops, tablets, car displays, and VR smart wearables. Although there are many diverse application scenarios, MiniLED is not always the best choice.

After years of market research, Qiu Yubin, the deputy general manager of TrendForce, analyzed that at present, the six major applications of MiniLED backlighting can be clearly distinguished.

In the applications of laptops and tablets, the development of MiniLED backlighting has shown some lack of momentum. In these two major application fields, Apple’s role as a trendsetter is particularly evident. MiniLED backlighting can be said to have officially entered the laptop and tablet markets under the influence of Apple’s brand effect, but due to high costs, Apple has recently clearly slowed down its pace of introducing MiniLED backlighting in laptops and tablets. At the same time, the threat from OLED is becoming increasingly significant.

Qiu Yubin pointed out that OLED manufacturers have determined investment in 8.5-generation OLEDs in order to achieve a higher level of economic cutting of notebooks and tablets this year, so that the cost of OLEDs is expected to continue to fall, and MiniLED backlights may continue to be in the downside. Qiu Yubin predicts that Apple is likely to use OLED screens on next year’s iPads, which means that Apple’s products will enter a period of drastic adjustment. In addition, after the adjustment of 8.5 generation OLED, Apple notebooks in 2025 also have the possibility of choosing OLED, in this context, the development of MiniLED backlights in notebooks and tablets will be more conservative.

In TV applications, the threat of OLED to MiniLED is relatively less obvious. First of all, looking at shipments, in 2022, the OLED TV market has encountered headwinds, with shipments of about 6.7 million units, an annual increase of only 0.5%, and it is predicted that there may be a 0.7% decline this year, with shipments of about 6.3 million units. In contrast, MiniLED backlit TVs will ship 3.5 million units in 2022, an annual increase of 65%, and it is estimated that MiniLED-backlit TV shipments will reach 4.4 million units in 2023, an annual increase of about 26%.

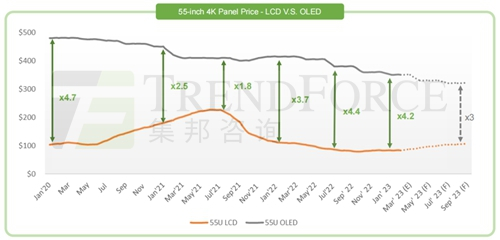

Looking at the situation of LCD, it still stands firmly in the mainstream position of TV panels, and continues to open the price difference with OLED, and MiniLED as a backlight improves the contrast, brightness and picture quality performance of LCD TV, which is equivalent to enhancing the competitiveness of LCD. In the long run, relying on the cost advantage of LCD panels, combined with the continuous breakthrough of its own technology and the gradual decline of costs, MiniLED backlights will continue to penetrate the TV market.

Monitor applications, OLED and MiniLED backlight displays are also in the initial embryonic stage, both have large room for growth, but in fact, the two have been superior in some aspects, which is mainly reflected in the supply chain.

In terms of panel supply, OLED shares suppliers and production lines on TV and Monitor applications, that is, panels produced by LG 8th generation lines are used, and production capacity is limited; The MiniLED backlight display supply chain has a complete industrial chain, especially in the domestic market. From the perspective of last year’s brand layout, according to TrendForce data, domestic brands accounted for 39% of the global Monitor market shipments, and it is expected that the proportion may increase to 70% this year. In this context, domestic brands will have high efficiency in product promotion and cost compression, which is expected to drive MiniLED to quickly penetrate the Monitor market.

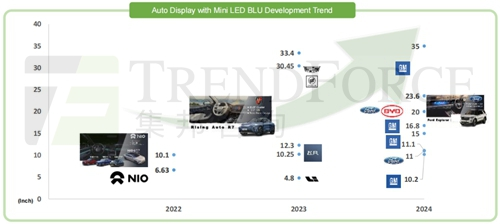

In the application of vehicle display, MiniLED officially opened the market under the introduction of the American brand Cadillac, and Chinese brands have spared no effort to accelerate the process of MiniLED “on the car”. Qiu Yubin pointed out that the advantages of LCD+MiniLED backlight solution in terms of reliability, brightness and contrast make it an ideal choice for in-vehicle displays, which can meet the needs of driving safety and driving experience at the same time. In terms of market layout, Chinese and American brands take the lead, and European and Japanese brands follow. TrendForce expects that after 2024-2025, Japanese and European brands will gradually join the layout camp of MiniLED-backlit car displays.

In terms of VR applications, last year, with the release of Meta’s first VR device equipped with MiniLED backlight technology, Meta Quest Pro, the market’s expectations for MiniLED-backlit VR devices have increased. However, according to TrendForce’s observation, the high cost of the device itself, combined with the combination of sensing components, the final price reached $1649, so the market feedback was not as expected.

As far as MiniLED backlight technology itself is concerned, it is not yet competitive enough in the field of VR headsets. On the one hand, the cost of MiniLED is still at a high level; On the other hand, in terms of thickness, lightweight, and energy saving, MiniLED is not as good as Micro LED. Combining the two key factors of consumer purchasing power and wearing comfort, TrendForce has a conservative view on the development of MiniLED backlights in this application field.

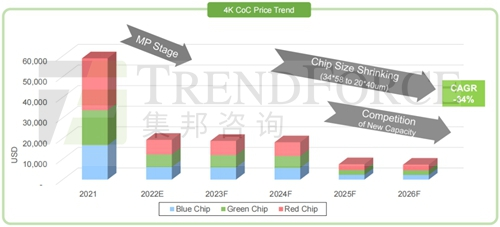

In the past two or three years, large-size displays have been the mainstream application of Micro LED, and accompanied by a high market voice, but the actual progress has not achieved the expected effect. Although the path of chip cost reduction is clear (it is expected to decrease by more than 30% per year, and the peak point of chip cost reduction will be reached in 2024-2025), TrendForce also conservatively views the development of Micro LED in large-size applications, specifically from two aspects: the relationship between yield and cost of other processes, the relationship between cost structure distribution and brand.

Micro LED large size good things grind, small size god stroke

Qiu Yubin introduced that the cost composition of Micro LED, in addition to chips, there are other links and processes, such as backplanes. Therefore, chip cost reduction alone is not enough to drive the overall cost reduction. Taking Samsung products as an example, The Wall is a Micro LED large display spliced by multiple modules and boxes, using a 12.7-inch LCD LTPS process substrate. Although the LTPS process is simple, in order to achieve seamless splicing, other processes such as side wires need to be added to the substrate, and the yield of such processes is currently relatively low, which poses great challenges to manufacturers and naturally produces higher costs.

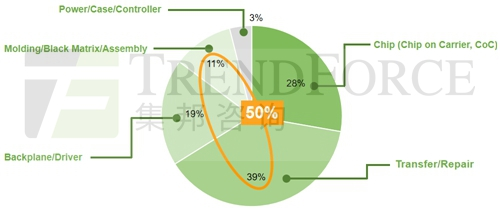

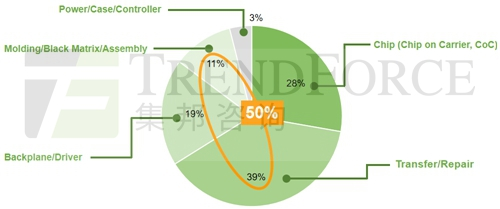

Looking at the distribution of the overall cost structure, according to TrendForce analysis, Micro LED cost structure includes five parts: chip (28%), transfer/rework (39%), backplane/driver (19%), molding/black matrix/assembly (11%), power supply/housing/control board (3%).

Qiu Yubin pointed out that the cost of transfer/rework, molding/black matrix/assembly accounts for more than half of the total, and the cost of these two parts is borne by the brand side, which means that the brand side needs a lot of investment, reserve and accumulation. In other words, for emerging brands, the learning curve and production yield experience in the field of Micro LED large-scale displays will be relatively high thresholds. At present, in addition to Korean manufacturers, other manufacturers may need a certain amount of time to brew, and after accumulating production experience, they can embark on a relatively good road.

In contrast, Micro LED small-size displays seem to have exceeded expectations.

For months, news of Apple’s Apple Watch dynamic predictions has been endless. Qiu Yubin analyzed that since the mass production of Apple Watch in 2015, subsequent versions have mainly worked on size, brightness, display area, and power saving, which are in line with the characteristics of Micro LED.

According to TrendForce research, before Apple releases Apple Watch next year, other brands are expected to be the first to release smart watches with Micro LED in the second half of this year, which is about 1.4 inches in size. Qiu Yubin believes that the release of this product is expected to become the starting point for Micro LED to officially knock on the door of the smart wearable field.

AR device displays are also a suitable entry point. In order to achieve the effect of light and transparent penetration, manufacturers currently choose optical waveguide technology, however, the conversion efficiency of waveguides to light is less than 1%. Looking at AR light engine technology, Micro LED has natural advantages over Micro OLED in terms of brightness and reliability, and therefore, many Micro LED AR alliances have been formed around the world, such as Meta+Plessey, Google+Raxium, Oppo+JBD and so on.

It is foreseeable that the application prospects of Micro LED in the field of AR display are beautiful, but based on the present, Micro LED needs to overcome many technical obstacles before achieving the ideal effect pursued by AR, including full-color problems, efficiency problems of red light chips, the choice of chip materials and structures, the choice of giant transfer and detection technology, the choice of backplane and driver architecture, etc.

The on-board display is a little far away, but it’s also worth looking forward to. Qiu Yubin said that the possibility of Micro LED in the field of automotive display is reflected in the future automotive demand for transparent screens, curly screens and even extended screens, observing the exhibitions in recent years found that panel manufacturers such as Yongchuang, AUO, Innolux, and Tianma have repeatedly shown the infinite possibilities of automotive Micro LED transparent screens to the market. Even if it must be a high-cost product in the future, the unit price of high-end vehicles is extremely high, in contrast, it can be expected that the high unit price of the whole vehicle has the opportunity to dilute the burden of Micro LED costs.

In general, the scene of the emerging application market of Micro LED is like the beginning of the lights, ready to go.

The road ahead is long but worth waiting

The fog gradually cleared, the road gradually cleared, and although the Mini/Micro LED has a long way to go, it will eventually usher in further growth.

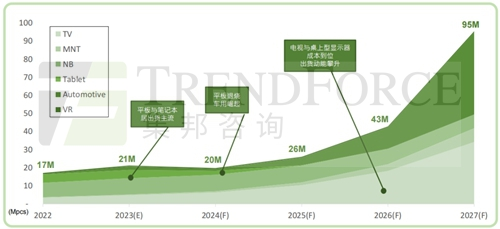

According to TrendForce’s “2023 MiniLED Backlight New Display Market Analysis Report”, shipments of MiniLED backlight application products will increase from about 17 million units in 2022 to about 21 million units in 2023. But it should be admitted that Apple’s iPad and MacBook have a great impact on the direction of the entire market, considering that Apple is likely to switch from MiniLED to OLED, TrendForce estimates that shipments of MiniLED backlight application products will decline in 2024. However, this will only be a turbulence phenomenon in the short term, and after 2024 and 2025, as costs fall, more brands will introduce MiniLED, and shipments are expected to reach 75 million units in 2027.

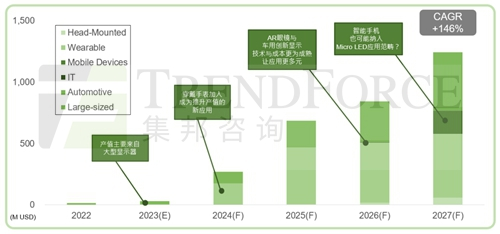

The growth curve of Micro LED is relatively unfluctuating, and it is expected to maintain year-on-year growth in the next few years.

According to TrendForce’s “2023 Micro LED Self-Luminous Display Cost Analysis and Development Trend Analysis Report”, in 2023, the growth momentum of Micro LED chip output value will still mainly come from large-scale displays, and the market size is expected to grow from about $14 million in 2022 to about $32 million. In 2024, wearable devices will become another engine to drive the growth of Micro LED chip production after mass production begins.

Looking forward to 2026, with the further maturity of technology and cost, AR and vehicle displays are expected to enter the fast lane of development, driving the demand for Micro LED chips. On the basis of a significant reduction in costs, it is bold to expect that smartphones will also provide opportunities for Micro LED applications in 2027. Considering the possibilities of all application scenarios, TrendForce estimates that the overall chip output value will reach $1.244 billion in 2027, with a compound annual growth rate of 146%. All in all, Micro LED has a wide road, and the application prospects are very worth looking forward to.